Karen#1

Well-known member

EXCERPT:

This is not a tax case. It’s not a theological debate. This is a forensic breakdown of a public document designed by David Miscavige to create the illusion of legitimacy and to protect himself.

In 1993, after years of litigation, harassment, and secret negotiations, the IRS granted tax-exempt status to Scientology. But what followed was a decades-long propaganda campaign weaponizing that exemption as if it were an unchallengeable endorsement. It wasn’t. And it still isn’t.

Devo’s Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

This post dissects Scientology’s official IRS exemption page line by line, screenshot by screenshot to reveal how Miscavige personally orchestrated the deal, misrepresented the truth, and continues to use the IRS ruling as a legal shield while violating nearly every standard that exemption requires.

We are not reviewing church doctrine. We are exposing a strategy of deception one that may ultimately unravel the very protection David Miscavige worked so hard to manufacture.

This is Part One of a two-part legal takedown. Each claim made by Scientology is measured against what we now know, and each section builds the evidentiary case: the fraud wasn’t just institutional, it was personal.

Screenshot #1 – The Illusion of Legitimacy: How Scientology Weaponizes the IRS Exemption

This opening statement is deliberately designed to mislead. It frames the IRS exemption not as a narrow, revocable administrative designation but as a blanket endorsement of Scientology’s legitimacy and structure. That framing is false, and legally dangerous.

The visual layout of government buildings and legal documents is crafted to evoke finality and governmental blessing, when in fact, the 1993 IRS exemption was the result of a private, secretive negotiation one that was personally engineered and controlled by David Miscavige.

As the self-appointed Chairman of the Board of Religious Technology Center (RTC), Miscavige took over all critical negotiations with the IRS in 1991. He personally removed all intermediaries, oversaw every legal maneuver, and ultimately signed off on the compliance commitments. He has since violated nearly every condition of that agreement, while publicly promoting it as proof of legitimacy.

Contradiction: Governance and Control

By identifying CSI as the “Mother Church,” this page invites scrutiny into its governance. But corporate records show CSI is a hollow shell, without a functioning board or executive autonomy. In reality, CSI’s decisions and operations have been entirely controlled by David Miscavige for decades, in direct contradiction of nonprofit law and the IRS Closing Agreement’s stipulations.

This means the IRS was misled and today’s readers are being misled into believing CSI operates as an independent religious entity. In truth, Miscavige has rendered it non-operational by design, centralizing all meaningful power under himself.

Legal Relevance

This screenshot now serves as documented evidence of David Miscavige’s personal use of the IRS exemption as a legal shield:

Evidentiary Use in Ongoing Casework

David Miscavige’s personal liability.

It directly supports:

Read More:

devodevocht.substack.com

devodevocht.substack.com

This is not a tax case. It’s not a theological debate. This is a forensic breakdown of a public document designed by David Miscavige to create the illusion of legitimacy and to protect himself.

In 1993, after years of litigation, harassment, and secret negotiations, the IRS granted tax-exempt status to Scientology. But what followed was a decades-long propaganda campaign weaponizing that exemption as if it were an unchallengeable endorsement. It wasn’t. And it still isn’t.

Devo’s Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

This post dissects Scientology’s official IRS exemption page line by line, screenshot by screenshot to reveal how Miscavige personally orchestrated the deal, misrepresented the truth, and continues to use the IRS ruling as a legal shield while violating nearly every standard that exemption requires.

We are not reviewing church doctrine. We are exposing a strategy of deception one that may ultimately unravel the very protection David Miscavige worked so hard to manufacture.

This is Part One of a two-part legal takedown. Each claim made by Scientology is measured against what we now know, and each section builds the evidentiary case: the fraud wasn’t just institutional, it was personal.

Screenshot #1 – The Illusion of Legitimacy: How Scientology Weaponizes the IRS Exemption

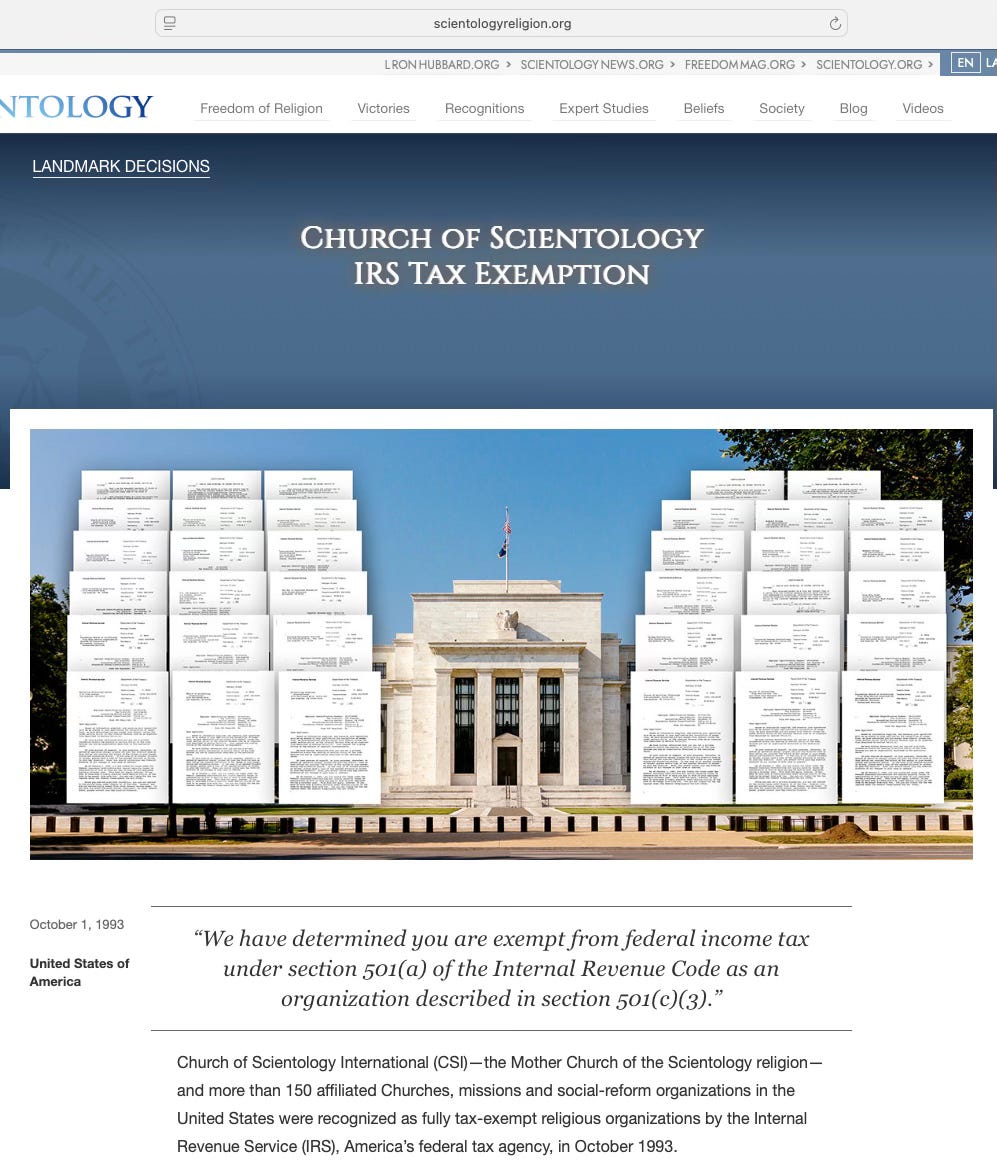

Legal Analysis“We have determined you are exempt from federal income tax under section 501(a) of the Internal Revenue Code as an organization described in section 501(c)(3).”

— ScientologyReligion.org (IRS Exemption Landing Page)

This opening statement is deliberately designed to mislead. It frames the IRS exemption not as a narrow, revocable administrative designation but as a blanket endorsement of Scientology’s legitimacy and structure. That framing is false, and legally dangerous.

The visual layout of government buildings and legal documents is crafted to evoke finality and governmental blessing, when in fact, the 1993 IRS exemption was the result of a private, secretive negotiation one that was personally engineered and controlled by David Miscavige.

As the self-appointed Chairman of the Board of Religious Technology Center (RTC), Miscavige took over all critical negotiations with the IRS in 1991. He personally removed all intermediaries, oversaw every legal maneuver, and ultimately signed off on the compliance commitments. He has since violated nearly every condition of that agreement, while publicly promoting it as proof of legitimacy.

Contradiction: Governance and Control

This is the legal pivot and the trap.“Church of Scientology International (CSI)—the Mother Church of the Scientology religion...”

By identifying CSI as the “Mother Church,” this page invites scrutiny into its governance. But corporate records show CSI is a hollow shell, without a functioning board or executive autonomy. In reality, CSI’s decisions and operations have been entirely controlled by David Miscavige for decades, in direct contradiction of nonprofit law and the IRS Closing Agreement’s stipulations.

This means the IRS was misled and today’s readers are being misled into believing CSI operates as an independent religious entity. In truth, Miscavige has rendered it non-operational by design, centralizing all meaningful power under himself.

Legal Relevance

This screenshot now serves as documented evidence of David Miscavige’s personal use of the IRS exemption as a legal shield:

- He led the negotiation that secured the exemption,

- He dissolved the governance structures it relied on,

- And he now promotes the exemption as proof of righteousness while committing inurement, obstruction, and fraud under its cover.

- Fraudulent Misrepresentation to the IRS and public,

- Private Inurement and Lack of Governance, in violation of 501(c)(3),

- Command Responsibility, as the entity named as “Mother Church” is inactive, while actual control resides with Miscavige,

- Violation of the 1993 IRS Closing Agreement, which required transparent governance and separation of powers.

Evidentiary Use in Ongoing Casework

David Miscavige’s personal liability.

It directly supports:

- Allegations of fraudulent misrepresentation by Miscavige to the IRS,

- Command responsibility for the hollowing-out of CSI and the failure of compliance,

- And public deception intended to intimidate critics, courts, and government agencies using the illusion of IRS validation.

Read More:

The IRS Myth, Part One: How David Miscavige Engineered a Legal Shield Out of Lies

Inside Scientology’s curated exemption page, and why it may now be the most legally incriminating document David Miscavige ever approved.

devodevocht.substack.com